The Volvo Group will shift focus from the South African market to other markets on the continent this year as the local economy lags and opportunity for growth emerge elsewhere.

This is according to

Torbjörn Christensson, President: Volvo Group Trucks Southern Africa at Volvo Group.

Addressing the media at the company’s annual press conference and luncheon last week, Christensson said the Group was committed to building a better network outside of South Africa and was looking to attract the interest of new importers in Zambia, Kenya, Tanzania and Uganda.

-

Torbjörn Christensson, President: Volvo Group Trucks Southern Africa at Volvo Group says it is becoming harder to convince Sweden to invest in South Africa as the rand slides and the perception of the currency sours.

Africa focus

Christensson added that, in the past, the group’s total sales outside of South Africa totalled around 10% of all the vehicles it sold. But the intention now was to get this figure to around 30%, as South African transporters expanded into Africa. He is optimistic about the export markets which, he explained, had growth potential – albeit from an admittedly low base.

While opportunities for the Group exist in Africa, particularly in East Africa, some commodity-reliant countries like Zambia and Angola have been obliterated by the global commodity crunch.

“In Angola, they have 6% of the market left. We used to sell almost 800 trucks in Angola a year. Last year we invoiced around 30 or 40 units. So, there are worse places to sell trucks than South Africa.

“What has happened in the last couple of weeks will hit importers tremendously.”

“We see growth potential [in Africa]. What we lose here we could gain outside South Africa if our plans are correct. We have signed agreements with new importers and are changing importers in Kenya, Tanzania and Uganda this year. We have quite a successful setup in Ethiopia where we are renewing our footprint. And we have set up a dedicated organisation focused on this,” he says.

The Group will launch the UD Quester into the rest of Africa in Q1/Q2 this year. “If you look at Renault [Trucks] we are expanding the brand into Africa. We have done some extremely good sales in South Sudan and Ethiopia last year and will continue to drive that.”

Local market

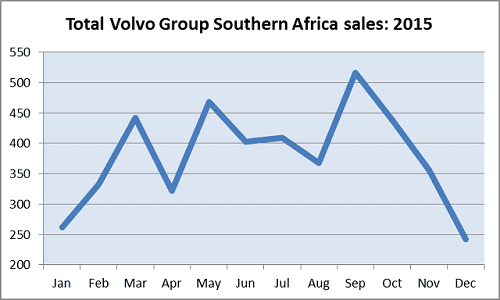

A single entity, Volvo Group Southern Africa comprises the brands Volvo Trucks, Renault Trucks and UD Trucks. In 2015 it commanded a 15% share of the total truck and bus market in South Africa, broken down as follows: Heavy duty segment: 24%; Medium duty segment: 21% and Bus segment: 6%.

-

The UD Quester launch, in April last year, was a “milestone” for the Group. A record 218 UD Trucks were sold in September last year.

“If you look at vehicle sales released by NAAMSA, [the total commercial vehicle market] declined by 4% and the heavy duty segment by 2%. We had a forecast of plus a few percent over 2014, so the market has not been as good as we anticipated. Looking forward, GDP growth is planned for 1% this year. We wish for higher, but this is what is predicted.

“If you look back; we had 15% of the total SADC commercial vehicle market last year, including 1% of the light duty market, which we have now left. Market share-wise we are quite happy.”

Growing concern

Christensson said the Group was concerned with the fortunes of the local currency. “The scope of it [the rand’s depreciation] is not yet fully known. We don’t know where the end of it will be or if it will bounce back. I think we have a problem with our international perceptions.

“The board are extremely cautious at the moment. We have done a lot of investment last year and I am confident I will not get the same this year. That money will not be allowed to be spent this year. Everybody wants to take a wait and see [approach] to see what is happening here. Uncertainty is affecting us. Importing things will be more expensive and [the] interest [rate] might be changed. Of course, our pricing will, over time have to be changed as well.

“To take a simple analogy, we have lost 15% of our salaries but are expected to find 5% more for our employees. The equation is impossible to balance at the moment. We are anticipating a rather tough year,” he said.

-

Rand depreciation has accelerated in recent months

“Our time for investments has passed. Into the future, we need to invest 30% outside of South Africa or more because we are building up the network. We will have to wait for one or two years. There are good markets like Ethiopia and Kenya, Tanzania, Uganda. But of course, the very oil and mineral economies are struggling. Two years ago Africa was the rising star. Now, perhaps, it is the rising star that moves a little slower.

“If you are in Sweden you don’t hear the good and the bad, you hear that Finance Ministers are coming and going from Monday to Tuesday, and you hear about strikes and other things. You don’t hear about the good fundamentals that actually exist in the market. But we try to tell them.”

“We fight for money to be invested here.”

Christensson described the situation in South Africa as complex. “Lately, there has been too much negativity stacking onto each other – that is what they evaluate. It is not an easy labour market. It’s not an easy market to invest in and there are visa problems and travelling restrictions. It is not set up to be the dream scenario for investors. Before it was easier to get money to invest, that is for sure. But our Board members are clever; they see that there are a lot of opportunities as well. We are here for the long-term. We have a good footprint,” he said.

The 2016 outlook

Describing the 2016 outlook as “flat”, Christensson said the Group was on a drive to lower its operating expenses and upskill its staff.

Apart from the Africa focus, the Group in 2016 would also pay greater attention to:

• Customer satisfaction

• Its finance solutions

• Staff training and development

• Dealer network support

• Customer uptime

“Our customers will not have an easy year. We will do whatever we can to help them as they drive their vehicles harder. We will launch a better finance product during the year because we have noticed the banks are less willing to lend people money to buy trucks,” he explained.

During 2015, the Group opened a new Truck Centre in Bloemfontein and a new dealership in

strategically important Harrismith between Durban and Johannesburg. The Group also expanded the Parts Distribution Centre, roughly tripling the size of it. It upgraded the Competency Development Centre (CDC) and opened a dedicated

Used Trucks Centre.

During 2015:

•

335 000 workshop hours were sold

•

2 100 people were trained in the Group’s CDC

• Over

1 000 used trucks were sold in the UTC

• Roughly

R100-million was spent in SA

-

Quality used trucks are proving popular

Christensson added that the company had achieved success in other areas of the business, such as with maintenance contracts and the aftermarket which, according to him, were growing. “This year we are reviewing our Volvo Trucks dealership facility in Durban, which will be revamped and/or expanded,” he indicated.

New products

Christensson said a new, medium duty product, based on the

UD Quester, would be introduced in the middle of this year. “For Volvo in South Africa, we have what I would call a minor facelift of the FH coming during the year.”

He said the Group had decided to stop importing Completely Knocked Down (CKD) units for assembly of Renault Trucks in Durban, due to the economic non-viability thereof. Renault Trucks have always been assembled CKD in the company’s Durban assembly plant and will now only be available as CBU. Volvo Trucks will continue to be assembled as CKD in Durban, while UD Trucks are assembled CKD in Rosslyn.

Although a single entity, Volvo Trucks, UD Trucks and Renault Trucks are run as separate companies and brands. Recent changes to the company’s

organisational structure resulted in a slight reduction in staff, from around 980 to 940, he said.

-

The Volvo FH 13-litre 440 6×4 is the single best-selling model in the SA

“We are in the finalisation stage of the UD Trucks medium range product. We are due to introduce it in mid-2016. We made the decision that we would not produce Renault CKD units here, but we sell them on as CBU’s and especially in the markets outside of South Africa, where Renault is quite a successful brand. We will continue to service and sell Renault Trucks but not build them locally. The volume is not economically feasible.”

The Group’s Durban assembly factory is not expandable and the UD facility in Pretoria is well positioned, so it is unlikely that the two would be combined under one roof.

Sinking feeling

Christensson explained that the Group’s mining customers had been the most severely hit by the commodity crunch. Conversely,

refrigerated transport and general cargo continued to thrive. “That sector includes some very professional customers which have replacement cycles and they are carrying on in the good and the bad times. We keep on eating, even in tough times. The construction sector will depend on infrastructure investments. That is where the government could be more active; investing in infrastructure projects.”

“We need to adapt to a new reality.”

On the topic of Chinese truck brands in Africa, he said: “There are a lot of Chinese trucks in Africa, especially if you go north. They arrive to work on Chinese [construction] projects. But many transporters are experienced with buying European used trucks. There is space for all of us. We have aftermarket support and parts backup etc. You need to do a calculation and see if it’s better to buy a little more expensive truck whose background you know or if you should buy three trucks and run two, with the other a spare.

“The more advanced the markets get, the more towards European products they will most likely go because it will be just-in-time, it will be about downtime, and other KPI’s that are important. We have a positive view of this but, of course, we will have to compete, but not on price. On the heavy side with longer distances, you need reliability,” he concluded.