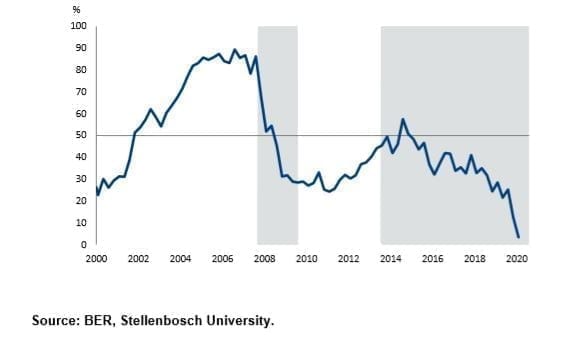

The FNB Bureau for Economic Research (BER) Building Confidence Index has fallen to an all-time low of 4 in the second quarter of this year, following the 13 recorded in the first quarter of the year.

The current level of the index indicates that almost all respondents are dissatisfied with prevailing business conditions.

Three sub-sectors registered lower confidence in 2Q2020, namely hardware retailers (-21), sub-contractors (-20) and main contractors (-13). Confidence of architects, quantity surveyors and building material manufacturers was unchanged at very low levels.

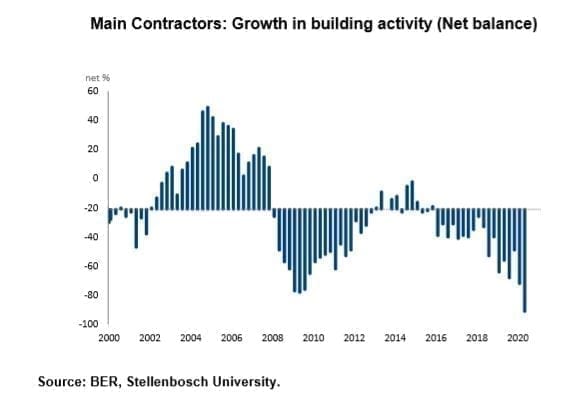

Main contractor confidence was at only 2 in 2Q2020.

In addition, the sub-index measuring building activity (relative to the same quarter in 2019) fell to its lowest level on record.

“With the vast majority of building contractors unable to work during April and May, it is unsurprising that activity tanked,” remarked Siphamandla Mkhwanazi, Property economist at FNB.

Looking ahead, based on respondents’ own expectations, activity is likely to contract again in 3Q2020 relative to a year ago. Moreover, order books also came under pressure as indicated by an increase in the rating of insufficient new demand as a business constraint.

“While a sharp fall in activity was expected in 2Q2020, the results raise an additional concern relating to the pace of recovery and the magnitude of activity in 3Q2020. Cancelled work and postponed tenders, as client firms go under or more aggressively manage cash flow, all argue for a prolonged period of depressed building activity growth. This means that the impact of the COVID-19-related shutdown will linger in this sector for some time. A quick recovery is most unlikely,” said Mkhwanazi.

The confidence of both architects and quantity surveyors was unchanged at 12 and 4 respectively. Activity remained very weak, although broadly in line with the 1Q2020 results.

This confirms the downbeat outlook for the building sector. According to Mkhwanazi, “the fact that activity didn’t deteriorate meaningfully – in fact, architect activity improved slightly – was largely as a result of different work arrangements in the case of architects and quantity surveyors who are able to work off site and from home. It also highlights just how unpromising the building pipeline already was in 1Q2020”.

Retailers of hardware registered the biggest fall in confidence, from 24 to 3 in 2Q2020. As expected, sales volumes fell dramatically in the quarter.

“The outlook for hardware retailers is bleak. Not only are they affected by slowing building demand, but falling consumer income is set to weigh heavily on this sector, at least for the remainder of this year,” added Mkhwanazi.

For similar reasons and as was the case in Q12020, further up the supply chain, not a single building material manufacturer was satisfied with business conditions in the second quarter.

At 4, the FNB/BER Building Confidence Index is at its lowest level on record. This was underpinned by a sharp fall in activity, understandably so given the nationwide lockdown in April and partial lockdown in May. An additional concern is that this quarter’s survey results point to continued weak activity next quarter.

“While we may see a rebound on a quarterly basis in 3Q2020 as a result of the gradual reopening of the economy, building demand (and therefore activity) is still going to be severely constrained over the short term. Even over the medium term, it is unclear that a full recovery is on the cards given how much damage the COVID-19-related lockdown has dealt to the property sector and how different behaviour, both individuals and business, may be in future,” noted Mkhwanazi.

The Nelson Mandela Bay Municipality has launched a pioneering partnership with the University of South Africa (UNISA) to dramatically expand access to library services for students and the broader public within the metro. Launched on Tuesday at New...

As South Africa implements the national rail reform programme, the private sector will play a key role in investing in rail and port operations, while ensuring that the infrastructure remains State-owned. “The current state of Transnet’s rail...

The National Minimum Wage Act 9 of 2018 (Act) was enacted to advance economic development and social justice by, inter alia, improving the wages of the lowest paid workers, and protecting workers from unreasonably low wages by establishing the...